Table of Content

If your phone, laptop or tablet is stolen from your home, downloads insurance will pay out for any lost digital content. We browse through a wide variety of coverages and find the right one for you.

We have mentioned a few riders earlier, but there are more like accidental death rider, accelerated death benefit rider, and income benefit rider. Now having too many choices puts you in a fix, making the buying process complicated. At times, having the right riders with a term plan can turn out to be more beneficial than a pure vanilla term life insurance.

What is downloads cover?

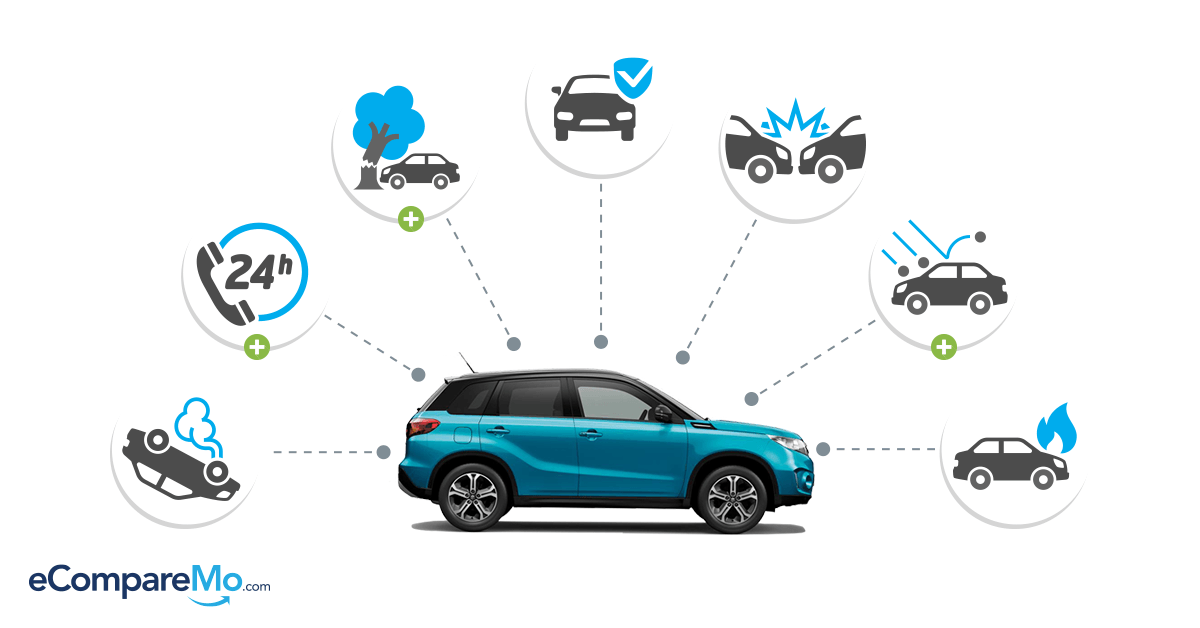

Lemonade is here for you 24/7 to provide our policyholders with fast customer support, online, and through our easy-to-use mobile app. Extended Reconstruction Cost add on offers additional coverage for cases where the cost of rebuilding your home ends up higher than expected. Lemonade offers Equipment Breakdown in AR, AZ, CT, GA, IL, MI, NJ, NM, OH, OK, OR, PA, RI, TN, VA, and WI—both for new policyholders and for those who are renewing a policy. You can add this endorsement to your Lemonade policy when you apply for a quote or on the app if you already have a policy. Legal services cover has a particularly low claims frequency of only 0.16%, highlighting how little is claimed on this obscure type of insurance cover. Recent FCA claims data shows that add-on services have a lower average claims cost as a proportion of premiums, compared to the corresponding standalone product, as seen from the table below.

Note that, add-on covers are designed to help policyholders in additional areas that the home insurance policy might not cover. Hence, choose only such home insurance add-ons that you think be applicable to your needs and circumstances. Homeowners Insurance protects us from many emergency situations, natural disasters, and theft. Add-ons, also called endorsements, floaters, and riders, help fill in the gaps. Endorsements allow homeowners to expand existing coverage where they need it most.Insurance policy add-ons allow homeowners to expand the list of covered perils in their coverage. For a small increase in premiums, policyholders can include benefits that were previously excluded from the policy.

important questions to ask when buying a property…

If your jewelry collection is worth more than that, you’ll need to purchase a scheduled personal property endorsement, known at Lemonade as Extra Coverage . No problem, you can get the big picture of your base homeowners insurance coverages here. For example, say at the time of the purchase of the policy, the critical illness rider came for a premium of Rs 4,200 per year, but the insurer might increase its rate after five years. This insurance is designed to help cover the cost of unexpected legal claims and disputes. It may be bought as a standalone policy or as an optional ‘add-on’ to other policies.

That’s in addition to any valuable jewellery you might also be wearing. However, restrictions apply, so check with the insurer before you buy. Also consider the excess for claims, and whether it would be worth you making a claim. Sinkholes — In Central Pennsylvania we are hearing increasing stories in the news about sinkholes. Depending on the geological composition of the ground on your property, your home and other structures could be susceptible to this catastrophe. Adding the sinkhole endorsement onto your policy will ensure that you won’t have to face the expense this can bring on your own.

Money

Accidental damage cover usually refers to one-off incidents - general wear and tear isn't included. Claims can be limited to relatively low amounts - sometimes just £500, which won't be enough to cover you if you need a new boiler. It's also debatable whether you even need boiler cover, given how rarely holders claim on it.

Basically, insurance add-ons are a great way to have some extra insurance coverage that better reflects your needs. They may become more or less applicable due to a change in your situation. The great benefit of them is that they are often more flexible than your basic insurance policy. Your individual insurance policy will dictate which add-ons you’re able to undertake. Here are 5 coverages that you can purchase along with your homeowners insurance policy to tailor it to fit you perfectly.

In most homeowners insurance policy, your home is covered against fire, theft, and damages. If you live in a flood or earthquake prone area, you may need to purchase additional coverage. Business insurance protects you and your small business against liabilities, unforeseen events, and the costs that come with them. These liabilities usually include accidents, personal injuries, property damage or a business service not having been rendered as advertised.

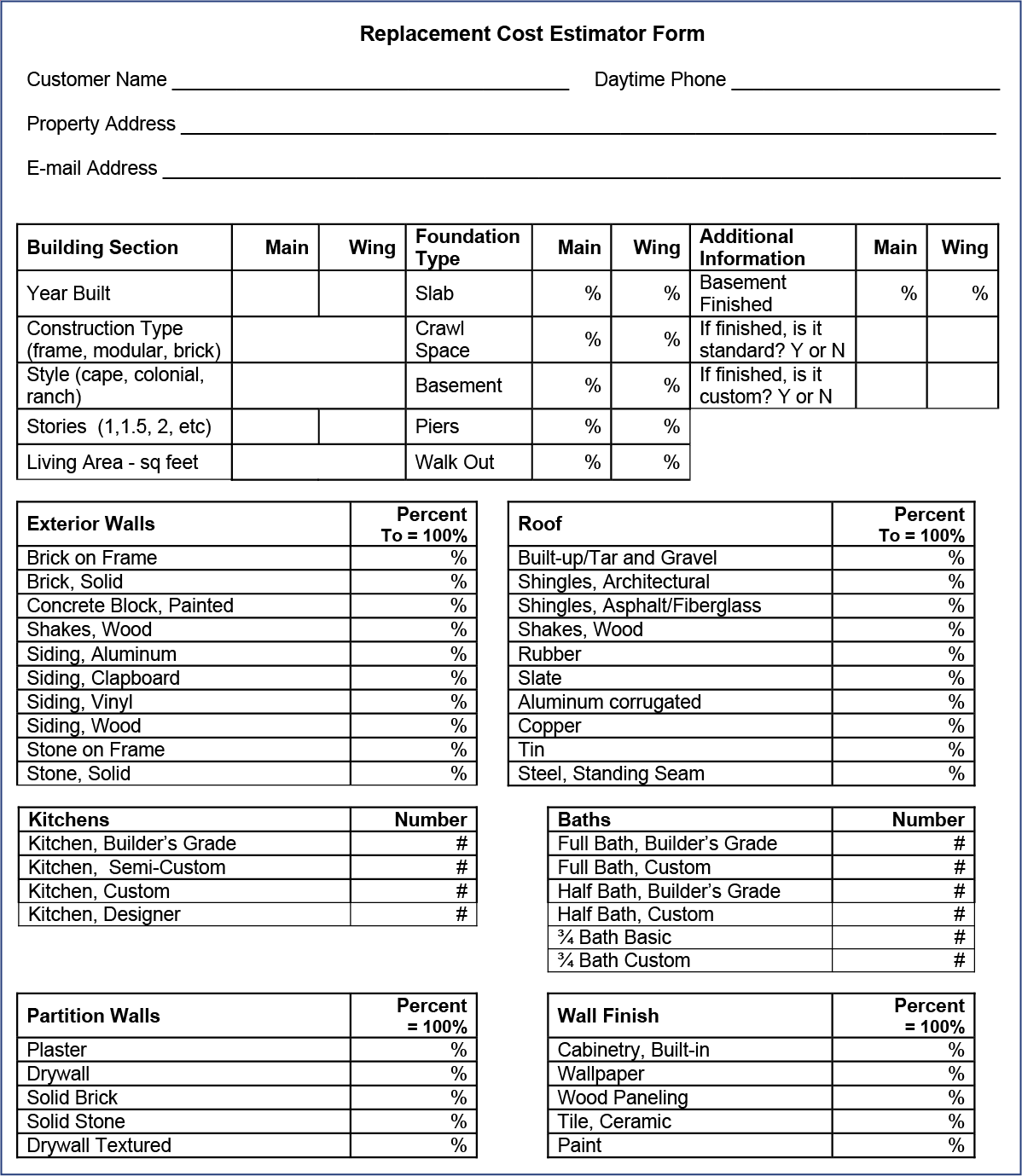

For example, you may have a valuable painting, high-tech computer equipment, or items related to your hobbies that are expensive to replace. Do not expect a standard homeowners insurance policy to cover these things if they are not specifically added to your policy. Whether or not it raises your costs depends on many factors, including how much value these items add. If not specifically included, and these items are lost in a fire, you could lose the financial value. You require flood insurance coverage since a typical home insurance plan doesn’t cover flood damage. Luckily, you can get flood damage coverage by purchasing a flood insurance policy from the National Flood Insurance Program or private insurers.

Yes, your home insurance covers high-value items like jewelry, art, and silverware, but the coverage is limited. As such, you need a rider to ensure you get total compensation for your high-priced assets when the unthinkable strikes. Water damage resulting from faulty sewerage isn’t covered by typical home insurance. While sewer and drain backups aren’t an everyday occurrence, they are inconvenient and expensive to fix when they occur. For this reason, you may need an endorsement to cover such damages. Let’s say a severe wildfire in Southern California consumes thousands of homes.

You can expect a rise of about 10% in your premiums with the Return to Invoice add-on. As you can see, no matter the condition of your vehicle, the value of the vehicle is going to depreciate based on the above calculations. Whenever you make a claim, the final amount you are compensated with is calculated after deducting the Depreciation on your vehicle. The percentage of Depreciation calculated based on the age of the vehicle has been elaborated below. All vehicles undergo wear and tear over time, and as a result of this, the value of the vehicle also drops. Be the first to hear about the best offers, promo codes and latest news.

No comments:

Post a Comment